- Loading...

IRS Release Status:FINAL

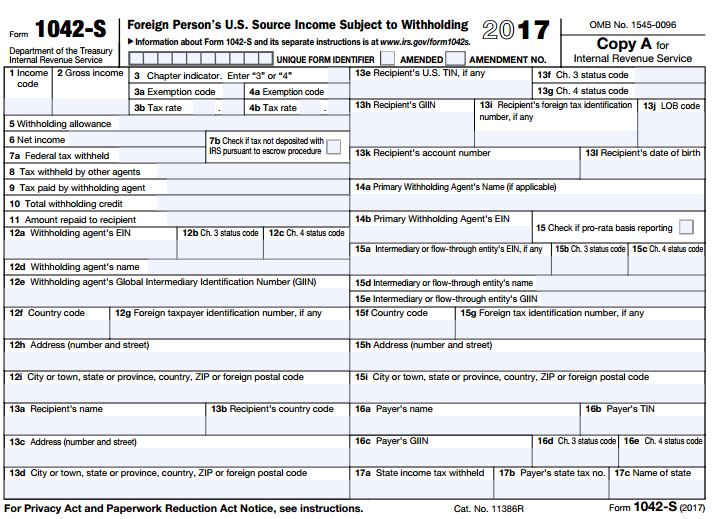

Sample Excel Import File: 1042-S

Import Form Fields:

| Field Name | Size | Type | Description | Notes |

|---|---|---|---|---|

| See Form Filer Common Fields | Filer fields common to all form types. | |||

| See Recipient Common Fields | Recipient fields common to all form types. | |||

| Unique Form ID | 10 | Numeric | Unique Form Identifier | A withholding agent must provide a unique form identifier number on each Form 1042-S that it files in the box provided at the top of the form. The unique form identifier must: Be numeric (for example, 1234567891), Be exactly 10 digits, and Not be the recipient's U.S. or foreign TIN. The 1042-S software will auto-assign Unique Form Identifiers if they are not included in the import file. |

| Box 1 Code | 2 | Text | Income Code | See IRS instructions |

Box 2 Amount | 12 | Amount | Gross Income | |

Box 3 Checkbox | 1 | Checkbox | Chapter 3 Indicator | X / Y / T / 1 = Checked |

| Box 3a Code | 2 | Text | Chapter 3 Exemption Code | See IRS instructions |

| Box 3b Number | 4 | Numeric | Chapter 3 Tax Rate | Tax Rate as a two-digit whole number and two-digit decimal |

| Box 4 Checkbox | 1 | Checkbox | Chapter 4 Indicator | X / Y / T / 1 = Checked |

| Box 4a Code | 2 | Text | Chapter 4 Exemption Code | See IRS instructions |

| Box 4b Number | 4 | Numeric | Chapter 4 Tax Rate | Tax Rate as a two-digit whole number and two-digit decimal |

| Box 5 Amount | 12 | Amount | Withholding Allowance | |

| Box 6 Amount | 12 | Amount | Net Income | |

| Box 7a Amount | 12 | Amount | Federal Tax Withheld | |

| Box 7b Checkbox | 1 | Checkbox | Check if tax not deposited with IRS pursuant to escrow prodecure | |

Box 8 Number | 12 | Amount | Tax withheld by other agents | |

| Box 9 Amount | 12 | Amount | Tax paid by withholding agent | |

| Box 11 Amount | 12 | Amount | Amount repaid to recipient | |

| Box 12b Code | 2 | Text | Withholding Agent's Chapter 3 Status Code . | See IRS instructions |

| Box 12c Code | 2 | Text | Withholding Agent's Chaper 4 Status Code | See IRS instructions |

| Box 13b Code | 2 | Text | Recipient's Country Code | See IRS instructions |

Box 13e TIN | 11 | Number | Recipient's U.S. TIN, if any | |

| Box 13f Code | 2 | Text | Recipient Chaper 3 status code | See IRS instructions |

| Box 13g Code | 2 | Text | Recipient Chaper 4 status code | See IRS instructions |

| Box 14a Name | 40 | Text | Primary Withholding Agent's Name (if applicapable) | |

| Box 14b TIN | 11 | Number | Primary Withholding Agent's EIN | |

| Box 15 Checkbox | 1 | Checkbox | Pro-rata Basis Chkbx | Pro-rata Reporting See IRS instructions |

| Box 15a TIN | 11 | Number | Intermediary flow-through's name | |

| Box 15b Code | 2 | Text | Intermediary’s or FTE’s Chapter 3 Status Code | See IRS instructions |

| Box 15c Code | 2 | Text | Intermediary’s or FTE’s Chapter 4 Status Code | See IRS instructions |

| Box 15d Name | 40 | Text | Intermediary/Flow-Through's Name | |

| Box 15e GIIN | 19 | Text | Intermediary or FTE GIIN | Global Intermediary identification Number (GIIN) |

| Box 15f Code | 2 | Text | NQI/FLW-THR/PTP Country Code | See IRS instructions |

| Box 15g TIN | 22 | Text | Recipient’s Foreign Tax I.D. Number | |

| Box 15h Address | 40 | Text | NQI/FLW-THR/PTP Address Line-1 | |

| 40 | Text | NQI/FLW-THR/PTP Address Line-2 | ||

| Box 15i City | 40 | Text | NQI/FLW-THR/PTP City | |

| Box 16a Name | 40 | Text | Payer's Name | |

| Box 16b TIN | 11 | Text | Payer's TIN | |

| Box 16c GIIN | 19 | Text | Payer's GIIN | |

| Box 16d Code | 2 | Text | Payer's Chapter 3 Status Code | See IRS instructions |

| Box 16e Code | 2 | Text | Payer's Chapter 4 Status Code | See IRS instructions |

| Box 17a Amount | 12 | Amount | State income tax withheld | |

| Box 17b State No. | 10 | Text | Payer's State Tax Number | |

| Box 17c State | 2 | Text | Payer's State Code | See IRS instructions |

| Form fields common to all form types. | ||||

1042-S Form:

IRS 1042-S Form: 1042-S Form

IRS 1042-S Instructions: 1042-S Instructions

1042-S Correction of a Correction Walk Through Guidebook PDF download

Overview

Content Tools