- Loading...

IRS Release Status: FINAL

Sample Excel Import File: 1099-B.xlsx

Import Form Fields:

| Field Name | Size | Type | Description | Notes |

|---|---|---|---|---|

| See Form Filer Common Fields | Filer fields common to all form types. | |||

| See Recipient Common Fields | Recipient fields common to all form types. | |||

| FATCA Checkbox | 1 | Checkbox | FATCA filing requirement | X / Y / T / 1 = Checked |

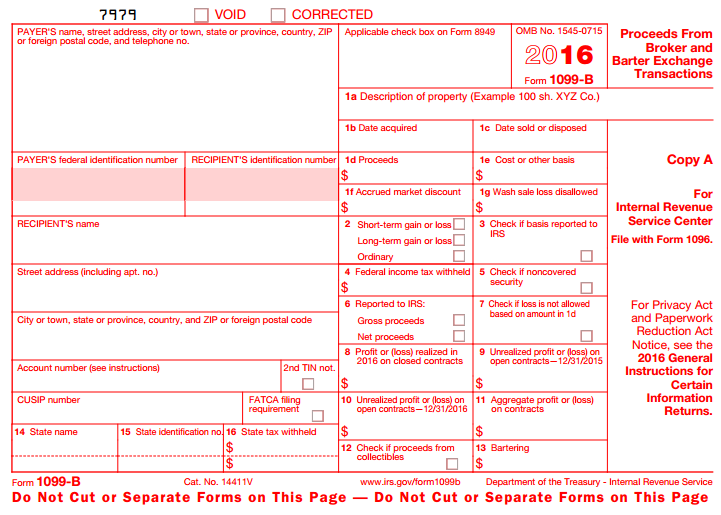

Box 1a Description | 45 | Text | Box 1a: Description of property | X / Y / T / 1 = Checked |

| Box 1b Date | 10 | Date | Box 1b: Date acquired | MM/DD/YYYY or M/D/YYYY |

Box 1c Date | 10 | Date | Box 1c: Date sold or disposed | |

Box 1d Amount | 12 | Amount | Box 1d: Proceeds | |

| Box 1e Amount | 12 | Amount | Box 1e: Cost or other basis | |

Box 1f Amount | 12 | Amount | Box 1f: Accrued market discount | |

| Box 1g Amount | 12 | Amount | Box 1g: Wash sale loss disallowed | |

| Box 2 Checkbox 1 | 1 | Checkbox | Box 2: Short-term | X / Y / T / 1 = Checked |

| Box 2 Checkbox 2 | 1 | Checkbox | Box 2: Long-term | X / Y / T / 1 = Checked |

| Box 2 Checkbox 3 | 1 | Checkbox | Box 2: Ordinary | X / Y / T / 1 = Checked |

| Box 3 Checkbox | 1 | Checkbox | Box 3: Check if basis reported to IRS | X / Y / T / 1 = Checked |

| Box 4 Amount | 12 | Amount | Box 4: Federal income tax withheld | |

| Box 5 Checkbox | 1 | Checkbox | Box 5: Check if noncovered security | X / Y / T / 1 = Checked |

| Box 6 Checkbox 1 | 1 | Checkbox | Box 6: Gross proceeds | X / Y / T / 1 = Checked |

| Box 6 Checkbox 2 | 1 | Checkbox | Box 6: Net proceeds | X / Y / T / 1 = Checked |

| Box 7 Checkbox | 1 | Checkbox | Box 7: Check if loss is not allowed on based on amount in 1d | X / Y / T / 1 = Checked |

| Box 8 Amount | 12 | Amount | Box 8: Profit or (loss) realized in 2016 | |

| Box 9 Amount | 12 | Amount | Box 9: Unrealized profit or (loss) on open contracts...2015 | |

| Box 10 Amount | 12 | Amount | Box 10: Unrealized profit or (loss) on open contracts...2016 | |

| Box 11 Amount | 12 | Amount | Box 11: Aggregate profit or (loss) on open contracts | |

| Box 12 Checkbox | 1 | Checkbox | Box 12: Check if proceeds from collectibles | X / Y / T / 1 = Checked |

| Box 13 Amount | 12 | Amount | Box 13: Bartering | |

| Box 14 State | 2 | Text | Box 14: State name | Use state abbreviation |

| Box 15 ID Number | 20 | Text | Box 15: State identification no. | Given by State Department of Revenue |

| Box 16 Amount | 12 | Amount | Box 16: State tax withheld | |

| See Form Common Fields | Form fields common to all form types. | |||

1099-B Form:

IRS 1099-B Form: 1099-B Form

IRS 1099-B Instructions: 1099-B Instructions

Overview

Content Tools